Novra Technologies Inc. (TSXV: NVI) (OTCQB: NVRVF) about to wake up?

Strong Q4 order book plus new investors/owners could position Novra for a strong 2025.

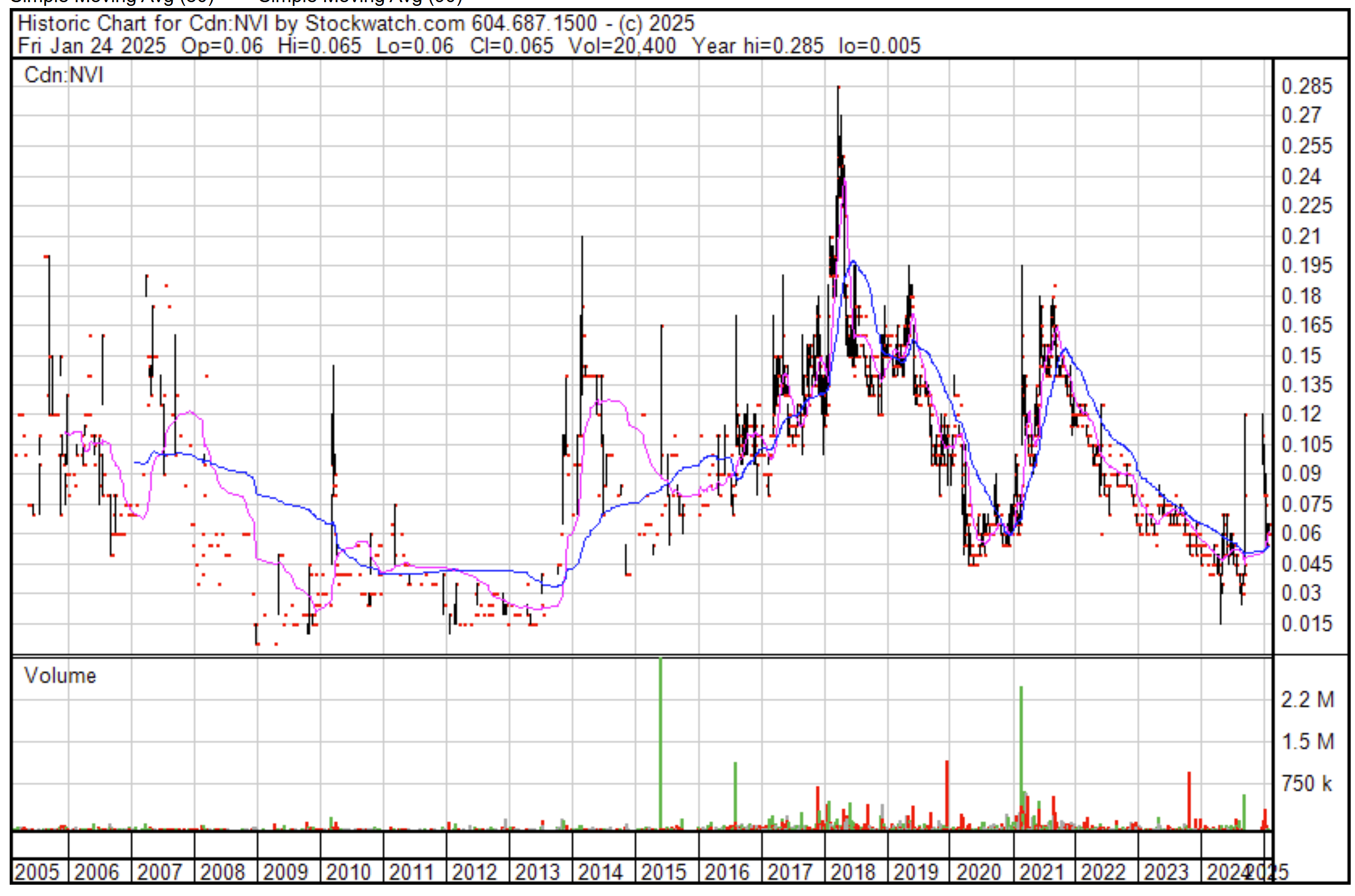

Novra Technologies is a microcap that has been around for 20+ years. During that time the stock has had a couple moments of brilliance but for the most part it has been dead money for 20+ years.

So why do I think this time will be any different? Well over the years they have acquired two additional companies International Data Corporation and Wegener. They have streamlined the businesses and are running as much leaner as a single entity. But that is not why I like this play.

Flash back to September 10 when Novra put out this NR: Novra Announces Convertible Loan Agreement of over $12M at $0.34 per Share. The stock went from .04 to .12 in a couple days before getting halted by CIRO “pending clarification of news”. Looking back, they were pretty naive to think this wouldn’t happen. I mean WTF. It’s not everyday you see a stock trading at .03 attract a US private investment group who is willing to invest $12M into a company with a market cap of $1.2M. Crazy! I’m surprised it took them 2 days to halt off this NR.

More than 2 months after the halt had commenced, Novra put out this news Novra Announces Significant Q4 Orders.

At the halfway point of our Q4, orders total over $2.3 million, close to the total combined bookings from the first three quarters of 2024

Now I am interested. I do not expect them to recognize this entire amount in Q4 but it does show that their customers are starting to spend again and this will provide a nice backstop for the share price going forward.

Fast forward to Dec 19 when Novra finally put our some clarifying news regarding their NR from 3 months back. Novra Announces Additional Details on Convertible Loan Agreement. This is where I really got interested and have been building my position since.

Let’s look at the NR.

Under this Convertible Loan agreement, Lender agrees to loan Novra $12.258 million for a term of up to two years at a fixed interest rate of 1.0% per annum. At its sole discretion, the Lender may elect to convert the outstanding principal balance of the Loan at any time during term to Novra common shares at a rate of $0.34 per share. At the end of the term, should the Lender not convert, Novra has the right to force the conversion of the outstanding Loan principal to shares at the same fixed rate, or to repay the loan. There is no finders fee associated with this transaction.

This was a deceptively written NR. If we do the math and divide $12.258M / $ 0.34 we get 36.052M shares. The company currently has 35.42M shares. The headline should have read, “SNAPS acquires majority ownership of Novra for $12.258M” because that is what has happened. SNAPS will own more than 50% of NVI if this transaction closes.

The closing date for this transaction has been moved to March 31, 2025. Now I fully expect this to close on that date, if not earlier. The downside protection we get is the solid upcoming Q4/Q1 numbers.

Who Is SNAPS?

SNAPS Holding Company (SNAPS), a privately held global enterprise headquartered in Fargo, ND with business interests in technology, manufacturing, healthcare, and commercial real estate (CRE) assets. With over 35 years of management history, SNAPS has a proven track record of successfully acquiring multiple hi-tech, mission-critical application companies worldwide. SNAPS is currently diversifying its portfolio by divesting some of its CRE holdings and reinvesting the capital in identified high-growth technology entities.

Seems like a legitimate company looking to diversify into “high-growth” technology entities.

SNAPS views Novra as a strategic asset, leveraging its global market reach, engineering excellence, SaaS/cloud proficiency, and wireless technology expertise. By investing into Novra, SNAPS aims to strengthen its position as a driver of innovation in the communications market with the addition of one or more of SNAPS' unique flagship products into Novra's technology arsenal to support its continued success at a much higher growth rate", said SNAPS' spokesperson.

Now we are talking. Over the past 20+ years Novra has built up its customer base and distribution channels. I have no idea what SNAPS’ unique flagship products are but adding those to the sales channel should be positive.

With SNAPS as the majority owner I think we will get a more focused, driven team behind Novra and it’s products. The current CEO, Harris Liontas, has been CEO of the company since June of 2002. He does not take a salary and according to my conversations with him, he does not need the money. This does not sound like a motivated CEO looking to increase sales. Let’s bring in a new motivated owner and see how far and fast we can push sales!

What Will Novra Look Like if This Transaction Closes?

Total shares: 71.47M

Market cap (@ $0.06): $4.29M

So, what about the $12M? Novra currently has just over $10M in liabilities from their acquisition of Wegener. My guess is that the funds will be used to pay off these liabilities and provide a one-time $1M payout to the CEO. This would leave the company debt-free, make the CEO whole, and position SNAPS to grow Novra at a much higher rate.

Let’s keep an eye on this transaction as we approach the March 31 closing date. If it doesn’t close, I believe the downside risk is mitigated by strong revenue growth over the next two quarters. However, if the transaction does close, the new ownership group will likely accelerate growth—especially if SNAPS’ flagship products complement Novra’s existing offerings. With Novra’s global customer base and a distribution channels, the potential for synergy is there.

I like this type of setup with illiquid stocks like these, as it allows me to sit on the bid and wait for impatient investors to sell it down. The way I see it, this will remain quiet until the end of the March/April timeframe, giving me a couple of months to slowly build up my position.

Using a horse racing stable analogy: You have your top horses, who race each week and bring in consistent paychecks, but you also have your yearlings, who aren’t ready to race yet but will one day be your top horses. Your stable should always be balanced so that the majority is earning money and supporting the stable, while a smaller portion of yearlings train and develop for future success.

This article is a follow up to my post, “The 2025 Microcap Meltup... Could it be?”

Disclaimer: Please note that I currently hold shares in Novra Technologies Inc, which may influence my perspective on the company and its related topics discussed in this content. I am not paid in any form from the company in this article or any other articles I have written.

If the loan closes and given the option of both parties to force a conversion at a share price of .34, SNAPS is valuing half the company at .34 given the number of shares that would be issued. I can only see the share price making a steady move towards .30 once the loan closes.

I would say it is incorrect to say that once the transaction (loan itself) closes the market cap would be $4.29M based on over 70M shares and a share price of .06.

This loan is taking longer due to time it’s taking for SNAPS to divest some CRE. Novra did receive an initial $500K USD tranche this week and expect more soon.